ET Intelligence Group: The stock of CreditAccess Grameen has gained nearly 12% over the past eight trading sessions after the country's largest microfinance lender announced the appointment of Ganesh Narayanan as the new managing director and CEO on August 6 after RBI's approval. The sector indices have gained over 1% during the period.

The company has undertaken accelerated write-offs to clean up the loan book, which has resulted in higher credit costs. The situation is expected to normalise from the December quarter.

Given the company's plan to open 200 branches in the current fiscal year and receding pressure on asset quality, the credit growth is expected to be higher in the second half of the current fiscal year.

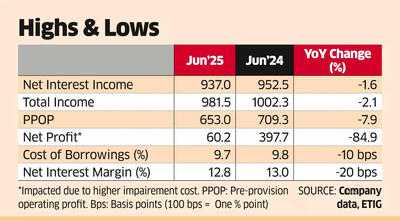

Dwindling credit quality in the microfinance segment over the past few quarters has affected the performance of CreditAccess. For its overall portfolio, 90-day PAR (portfolio at risk ratio) shot up to 3.3% from 1.1% in the year-ago quarter. The company has suffered a greater asset quality stress in Karnataka, which accounts for nearly one-third of its loan book. The PAR ratio for Karnataka in the 90 days and above category increased to 5.1% in the June quarter from 2.4% in the previous quarter.

According to the company management, Karnataka has started showing stabilisation in PAR in the current quarter. In addition, the implementation of stricter norms for loan disbursement has reduced the proportion of highly leveraged borrowers (which have borrowed from three or more lenders) to 11.4% in June from 25.3% last August.

The credit cost increased to ₹571.9 crore in the June quarter from ₹420.1 crore in the September 2024 quarter. This was largely due to accelerated write-offs as the proportion of new PAR accretion in the credit cost fell to 61% from 90% during the period. This raises hope that credit costs may ease in the second half of the current fiscal year.

Apart from asset cleanup, the company has also increased focus on retail financing, which is likely to form 12-15% of the loan book by FY28. The segment contributed 7% to the gross loans in the June quarter compared with 3% in the year-ago quarter.

Axis Securities expects annual growth in loan book and net profit at 18% and over 50% between FY25 and FY28. It has raised target price to ₹1,485 from earlier ₹1,350, implying FY27 expected price-book multiple of 2.5. Stock was last traded at ₹1,351 on Tuesday on the BSE.

The company has undertaken accelerated write-offs to clean up the loan book, which has resulted in higher credit costs. The situation is expected to normalise from the December quarter.

Given the company's plan to open 200 branches in the current fiscal year and receding pressure on asset quality, the credit growth is expected to be higher in the second half of the current fiscal year.

Dwindling credit quality in the microfinance segment over the past few quarters has affected the performance of CreditAccess. For its overall portfolio, 90-day PAR (portfolio at risk ratio) shot up to 3.3% from 1.1% in the year-ago quarter. The company has suffered a greater asset quality stress in Karnataka, which accounts for nearly one-third of its loan book. The PAR ratio for Karnataka in the 90 days and above category increased to 5.1% in the June quarter from 2.4% in the previous quarter.

According to the company management, Karnataka has started showing stabilisation in PAR in the current quarter. In addition, the implementation of stricter norms for loan disbursement has reduced the proportion of highly leveraged borrowers (which have borrowed from three or more lenders) to 11.4% in June from 25.3% last August.

The credit cost increased to ₹571.9 crore in the June quarter from ₹420.1 crore in the September 2024 quarter. This was largely due to accelerated write-offs as the proportion of new PAR accretion in the credit cost fell to 61% from 90% during the period. This raises hope that credit costs may ease in the second half of the current fiscal year.

Apart from asset cleanup, the company has also increased focus on retail financing, which is likely to form 12-15% of the loan book by FY28. The segment contributed 7% to the gross loans in the June quarter compared with 3% in the year-ago quarter.

Axis Securities expects annual growth in loan book and net profit at 18% and over 50% between FY25 and FY28. It has raised target price to ₹1,485 from earlier ₹1,350, implying FY27 expected price-book multiple of 2.5. Stock was last traded at ₹1,351 on Tuesday on the BSE.

You may also like

Afghanistan bus accident: Over 50 killed, including 17 children, after vehicle collides with truck, motorcycle - video

Mum's 'nightmare' ordeal after Hertfordshire Police Marcin Zielinski steals her underwear

Stains instantly disappear from clothes with 1 surprising kitchen item

The UK's smallest city is so tiny you can explore its pretty streets in 4 hours

The 'powerful' war film that's got a perfect 100% score on Rotten Tomatoes